For Millennials seeking to become homeowners, level of education may be more of a determining factor than any other socioeconomic indicator, according to a newly published white paper.

The study by Fannie Mae comes as the industry seeks to understand what is holding Millennials back from homeownership. The current generation of 18-to-34-year-olds is more likely to be living with their parents than in any other living situation for the first time in 130 years, according to a recent study by Abodo.

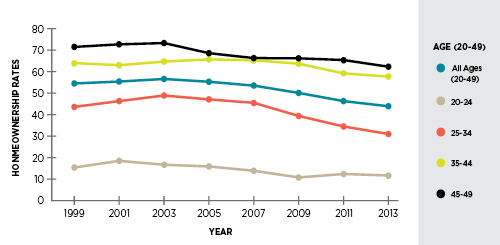

Millennials have not only been priced out of many urban markets, they also were more directly impacted by the Great Recession and housing market collapse of 2007, according to Fannie Mae’s study. In 2009, the last year of the recession, the overall unemployment level was 9.4 percent, but for Millennials it was 9.9 percent. The Millennial decline in homeownership was the greatest dip of any demographic during the market collapse: there was a 16 percent dip in Millennial homeownership from 2005-2013. (The second highest dip was 9.6 percent for those aged 35-44.)

There is a portion of the Millennial population that is buying homes, however. It turns out that education level — or the income and knowledge it affords — has an impact on a young person’s ability to buy a home, according to Fannie Mae.

This chart shows homeownership rates by age group. (Source: Fannie Mae)

Education’s effect on homeownership

Having a bachelor’s degree has always translated into a greater likelihood of home ownership, but even more so after the recession. Millennials with a bachelor’s degree are 9 percent more likely to own a home compared to those without a high school diploma, Fannie Mae reports.

What is it about being well educated that translates into homeownership? It’s true that college graduates are saddled with student loan debt and like to live in expensive urban centers. But holding a bachelor’s degree is also an indicator of other factors that might positively impact homeownership.

Higher levels of education could be a proxy for a more permanent income, Fannie Mae suggests. It could also be a stand-in for financial literacy that aids in buying a home.

“This post-recession era may have increased the importance of a household’s own education and income in determining its homeownership status,” the white paper reads. “In other words, in the wake of the Great Recession and housing bust, lenders might have placed a higher premium on educational attainment – and the boost to expected lifetime wages and employment stability that it typically brings – in determining who received a mortgage.”

Race plays a factor

Race still plays a determining role in who buys homes, according to Fannie Mae’s work. Young, Black Americans are less likely to own homes than whites, while Hispanic homeownership rates are on par with whites. And while education level plays a role in each race’s ability to purchase a home, the study shows that is more a determining factor for whites.

Prior to the recession, holding a bachelor’s degree increased a black person’s likelihood of homeownership by 8.5 percent. Post-recession, the number rose to 11 percent, a jump of nearly 3 percentage points. For whites, the jump was 6 percentage points: having a bachelor’s degree increased homeownership likelihood by 12.4 percent after the recession, compared with 6.1 percent before the recession.