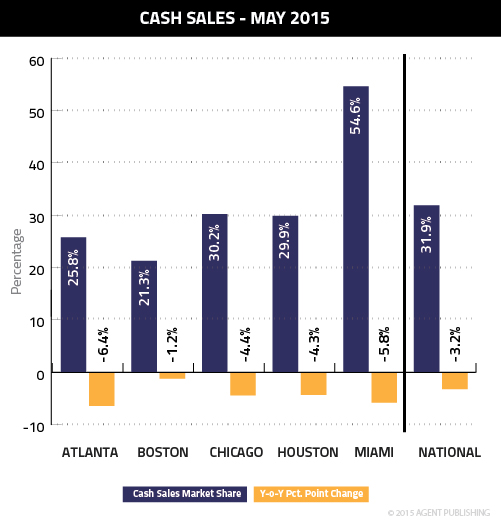

National cash sales continued their descent in May, a new report released today from CoreLogic showed.

For 29 months, all-cash buyers have been leaving the market, as marked by continual year-over-year decreases in market share. In May, cash sales made up 31.9 percent of total home sales, compared to 35.1 percent during the same time last year.

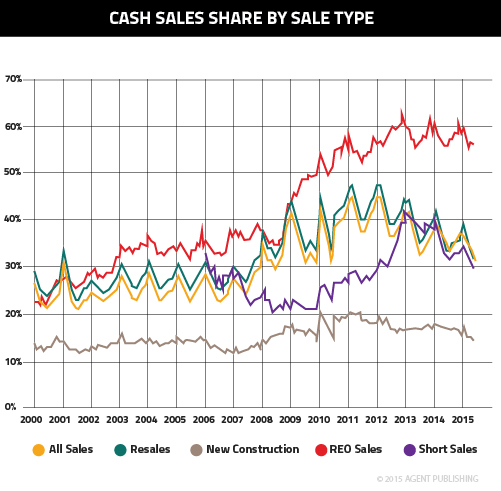

As the below graph shows, total cash sales share peaked in Jan. 2011, and have since been inching their way back down to “normal,” pre-crisis levels of around 25 percent. May’s dip was another step toward more stable cash sales levels, but as we move into fall and later winter, that number could come back up a little bit, as has been the case in years past.

In Georgia, where the cash sales share has dropped to 28 percent, the state is surging passed its neighbors, which all support levels above 30 percent – and Alabama and Florida above 40 percent. A big driver behind the state’s improvement has been the progress made by Atlanta in recent years. From May 2014, cash sales share in the Dogwood City have fallen 6.4 percentage points to 25.8 percent – one of the lowest in the nation. The drop in cash transactions represents an increase in traditionally financed home purchases and, ultimately, a more sustainable market.

Why is the market more sustainable when there is a increase in traditionally financed home purchases?

I agree with the above, you don’t get to say an increase in the use of debt to buy homes makes for a more sustainable market.

Jan the argument is probably that investors are more likely to be making all cash buys so as those decline more purchase are actually people buying to live in. So that means as more purchases are financed more homes are being bought by people who will use them as a primary residence, meaning the turnover of inventory is more stable because investment turnover will eventually decline because the investors are ‘fully invested’.

This has some flaws. Mainly assuming investors are all in vs no longer believe housing a good investment. If home demand is falling then pricing will follow. Maybe not to decline but probably stabilize until interest creeps up. It also assumes all cash is investor buying, I would like to know what percent of second/investment homes is actually all cash since I think it is lower than what people assume.

It could mean prices are unsustainable so investors are fleeing.